State of OpenCloud Report Deep Dive

The Folks at Battery Ventures put out a great annual report on cloud and open source software, its worth a read yourself but here's some things that jumped out to me!

Happy New Year readers! My first post was March 1st and my last post of 2021 was August 30th. Since then I moved across the country (from NYC to LA) and did a small thing…

I apologize for the delay in posts but the normal weekly schedule shall now resume! I think the wedding is as valid an excuse as any :)

In the meantime, the reader base has grown to 1,062 people!! I can not say enough how much it means to me that you all subscribe and hope to continue to deliver valuable snack bites (< 5 min reads) into your inboxes weekly.

Every year I look forward to Battery’s State of OpenCloud Report and the 2021 one was no exception! Below are a few slides that I thought were particularly interesting and my takeaways. Looking forward to all of your comments, emails, suggestions.

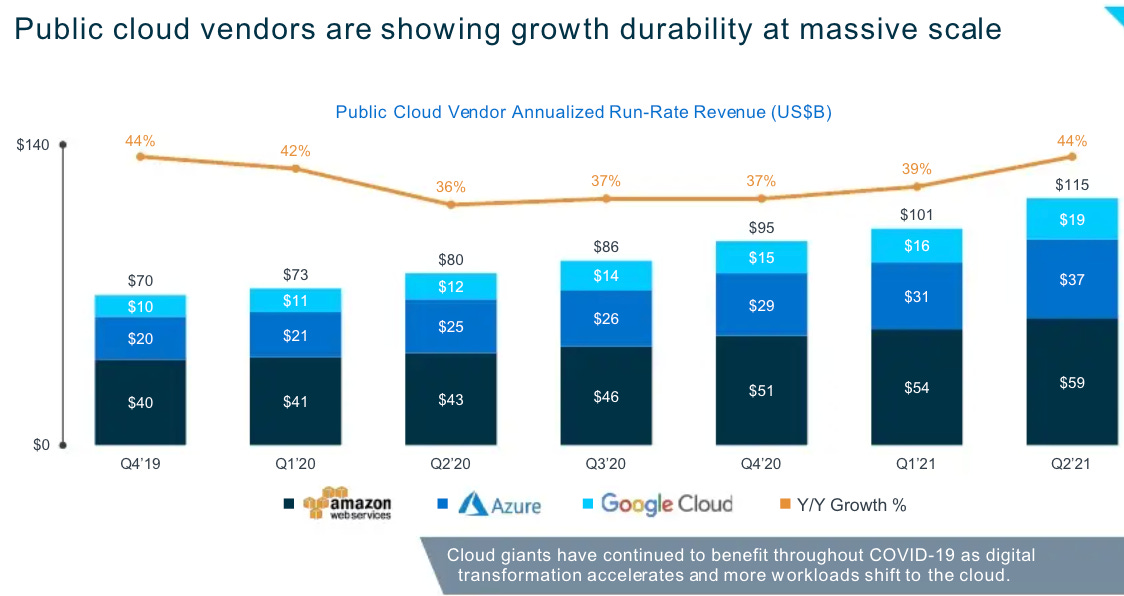

The scale of the cloud providers is insane especially as they continue to accelerate at massive scale. AWS is at a $64B run-rate in the current quarter, 39% YoY growth. In 2020, Gartner reported total IT spend to be $3.87T. That means even at AWS’ scale, it still only accounts for 1.7% of total IT spend. To say there is still room to run is an understatement.

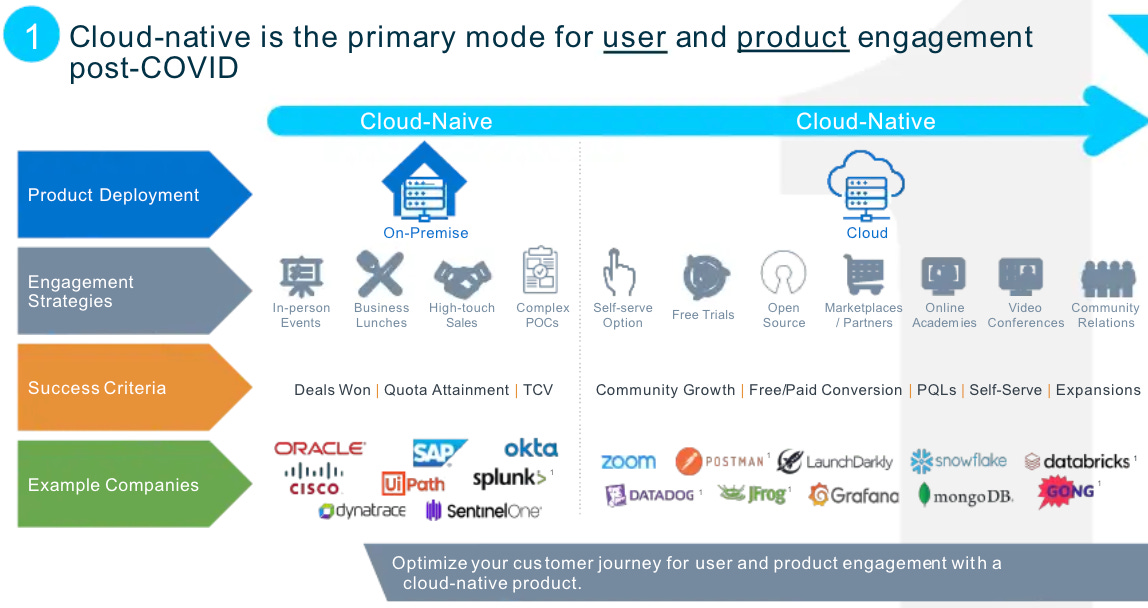

What’s driving the growth at so many of these companies? Delivering a cloud, fully managed service is increasingly the de facto way that customers are looking to purchase software. For a number of solutions, customers no longer want the hassle of managing updates and provisioning resources as usage grows. That enables cloud solutions to scale rapidly with the customers creating remarkable growth at scale while delivering tons of value to the customer.

Notice the companies mentioned on the left of this chart vs the right. It’s a good example reinforcing the point just made in the Cloud Growth photo above. The craziest thing about the Cloud-First companies is the adoption initially based on end users then matriculating to enterprise level contracts. You almost have consumer like dynamics to software infrastructure products which is a huge paradigm shift. Contrast this with the companies on the left which convince an executive to buy the product for the whole team. Very different motions some of which are becoming even more important in a covid world with remote workers and less centralized time together to chat about software purchases at large orgs.

The paradigm shift described in the paragraph above leads to product design & messaging increasing in importance. As end users are the first ones to try and champion these products within their orgs to eventually convince the budget owner to buy, messaging and ergonomics around the product matter more. The screenshots above provide examples of the best end user adopted products. My particular favorite is Snyk’s Quick Time to Action which is so clear for any end user “Find and fix vulnerabilities in 5 minutes”.

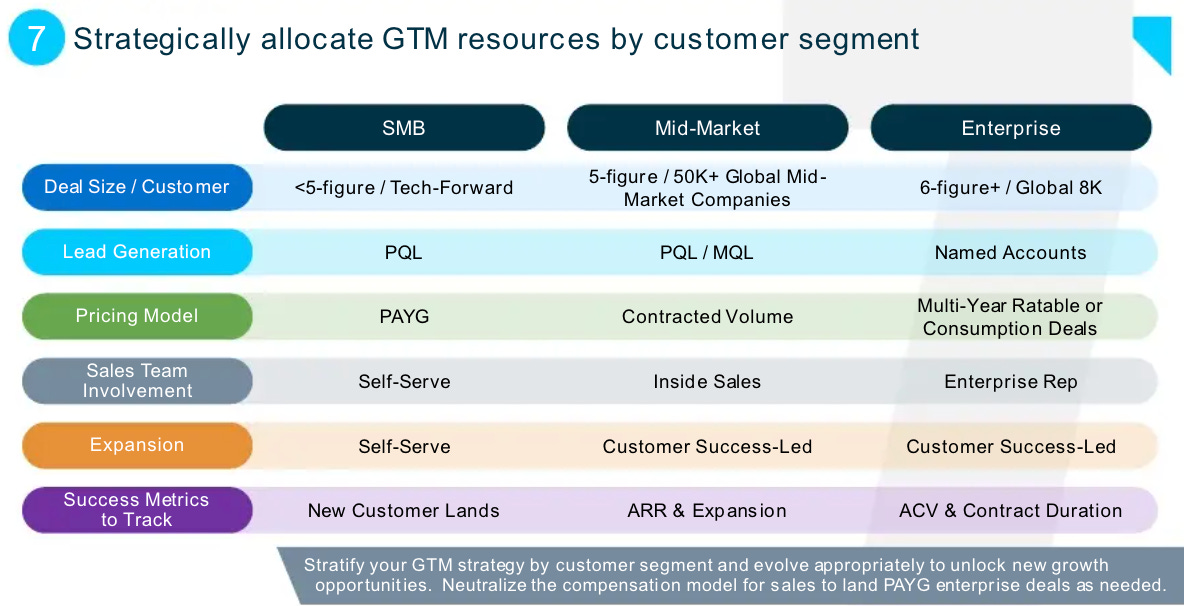

For frequent readers of this newsletter, I constantly preach about alignment of cost structure. The above chart is a great example. While everyone has recently been talking about product led growth, for Enterprises you still need traditional field sales. It requires relationships, enablement, careful navigation of various stakeholders and pitching org wide benefits. That is much different than what is needed or even works for SMB or many mid-market customers. For example, when I buy software at our <10 person org, I want to have a 30 min call to learn the value and instrument the product. Then I want some base level support for technical issues and that’s it. If someone was constantly asking for 30 min syncs every week, it would drive me crazy. Meanwhile as an enterprise, I would require multiple calls with various stakeholders plus 24/7 technical support for various timezones and much more. Those are very different needs!

While the multiple the companies get that are usage based is higher than subscription based, the flip side is you can still build a very valuable traditional SaaS business. For example, Salesforce, Workday, ServiceNow which are currently the most valuable enterprise software companies in the world are traditional subscription based. Meanwhile Datadog, Atlassian, and Snowflake are joining the ranks by being consumption based. Different methods but same outcome. Once again it comes back to aligned cost structure and solving the buyer’s problem. If you’re selling an enterprise firewall which affects a broad number of stakeholders then that will most likely be a single contract with modules added over time (Crowdstrike model). If you’re selling monitoring/logging for software, then an individual or team can gain more value from using the product more over time which aligns with consumption based pricing. Just like gtm, pricing needs to align to both product and gtm.

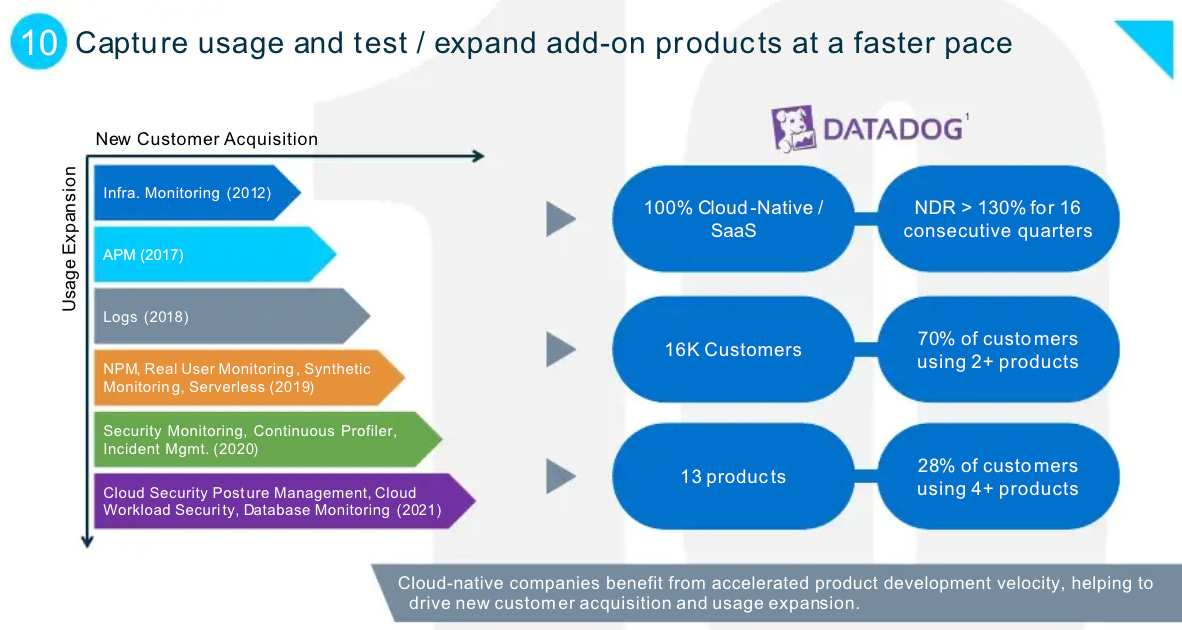

The best companies regardless of if they have consumption or subscription based pricing figure out how to solve adjacent customer pain points to deliver more value to each customer. One of the best case studies of this is Datadog which IPO’d at $12B and today is worth $50B. The pic above shows that Datadog moved from 1 product for quite a long time into an ever increasing rapid cadence of products as customers requested more features and as the company evaluated what adjacencies made the most sense with their current products & gtm to move into. This allows for Datadog to continue growing >60% at close to $2B ARR!

Look forward to reading y’all comments, emails or feel free to forward to any others who you think may like to be subscribers. Cheers to a great 2022!!

Congrast! 💚 🥃

Nice Picture from your Wedding , Interesting insights , Looking Forward !!!